Close

CloseEurope’s electric vehicle (EV) market had a resurgent period in the first six months of 2025. But which brands have been able to capitalise on this growth? Autovista24 journalist Tom Hooker goes through the figures from EV Volumes.

EV sales continued to climb in Europe across the second quarter of 2025, according to EV Volumes’ data. A total of 948,203 plug-ins were handed over to customers from April to June, marking a 27.4% year-on-year increase.

So, across the first half of 2025, EV deliveries grew by 23.8% compared to the same period last year. A total of 1,796,162 EVs were sold, equating to a gain of 345,691 units.

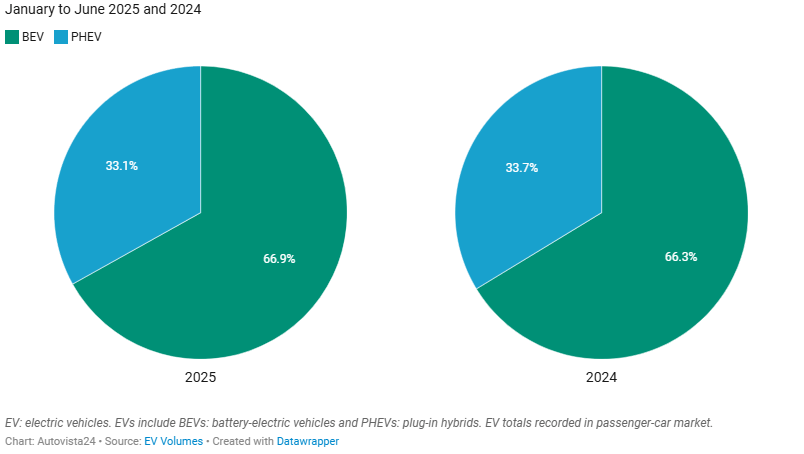

Plug-in hybrids (PHEVs) increased their share of the EV market in the second quarter. The technology accounted for 34.4% of deliveries, up by 2.8 percentage points (pp) year on year. This meant battery-electric vehicles (BEVs) represented 65.6% of sales.

BEV and PHEV shares of European EV market

However, across the first half of 2025, the share of BEVs within the EV market grew by 0.6pp to a dominant 66.9%. Consequently, PHEVs made up 33.1% of total deliveries.

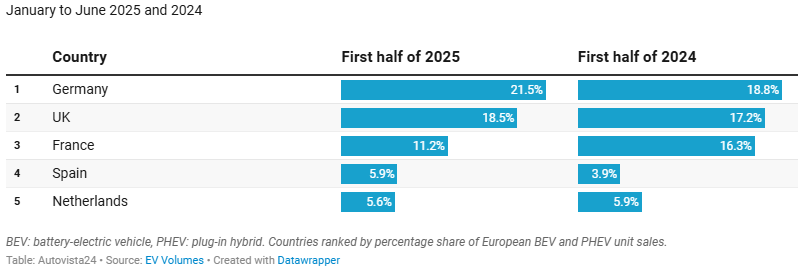

Germany leads Europe

Germany recorded the most EV sales in Europe from January to June. It accounted for 21.5% of all plug-in sales in the region, up 2.7pp year on year. The UK also posted high volumes, representing 18.5% of the European EV total, an increase from its previous 17.2% share.

Leading European EV markets by country share

France was third, making up 11.2% of overall deliveries. However, this was a significant drop of 5.1pp compared to the first half of 2024. Spain was some way behind in fourth with a 5.9%, yet this was a positive progression from its previous 3.9% market hold.

The Netherlands recorded the fifth-highest number of EV sales in the first half. Its 5.6% share was down by 0.3pp from the same period in 2024.

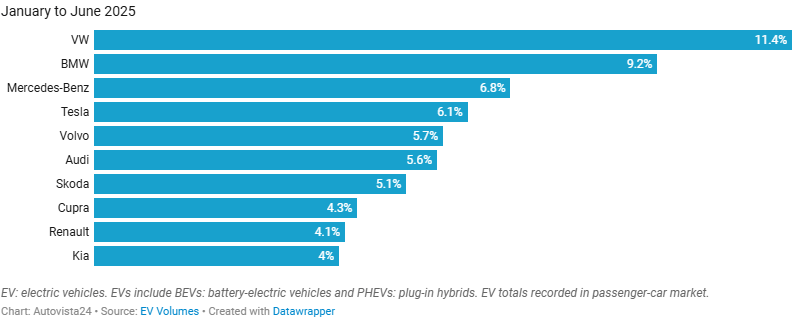

VW’s emphatic EV victory

Volkswagen (VW) led Europe’s EV market six months into 2025. Its market share soared from 6.5% during the same period of 2024 to 11.4% this year.

Leading brands by share of European EV market

This was thanks to the brand more than doubling its delivery total. Specifically, 204,805 units were handed over to customers, up 115.8% year on year. The German brand was also the best-selling carmaker in the second quarter.

VW has seen success in both the BEV and PHEV markets. Three of its ID. models featured in Europe’s all-electric top 10 from January to June, making up 56.5% of the carmaker’s EV sales. Meanwhile, its Tiguan SUV led the region’s PHEV market.

VW’s impressive performance has come at the expense of its two domestic rivals, BMW and Mercedes-Benz.

The former still sat in second, however, its market share fell by 0.7pp to 9.2%. This was despite posting a 15.1% sales growth, equating to 164,976 units. The brand enjoyed a solid performance in the second quarter, posting a 17.3% volume improvement.

The iX1 BEV was the manufacturer’s best-selling EV, accounting for 18.8% of its total in the region. The i4 BEV and X1 PHEV also made notable contributions to volumes, recording 14.2% and 12% shares, respectively.

Meanwhile, Mercedes-Benz suffered a 3.5% drop in volumes. The marque’s 121,986-unit total equated to a 6.8% share, down from 8.7%. This decline was driven by an 8.1% fall in sales during the first quarter. However, the brand recovered to record 1.5% growth from April to June.

The carmaker’s two best-selling EVs were the all-electric EQA and EQB. These models represented 16.9% and 14.1% of Mercedes-Benz’s European EV sales, respectively. Its GLC PHEV recorded significant deliveries too, representing 12.9% of the brand’s EV sales.

Contrasting EV fortunes

Tesla finished fourth in the first half of 2025. The US brand endured a 33.4% year-on-year sales decline, with 109,985 deliveries. Many parallels can be drawn between this result and VW’s turnaround.

In the first half of 2025, Tesla took a 6.1% European EV market share. This was 0.4pp below VW’s share at the same point last year. In the first half of 2024, Tesla led the market, representing 11.4% of regional EV sales. This is the same share that VW now controls.

Fifth place went to Volvo, which is struggling to match its 2024 performance. In the first half of 2025, volumes were down 17.2% to 102,533 units, while its share dropped by 2.8pp to 5.7%. The Swedish carmaker saw an even sharper sales decline of 20.9% in the second quarter, putting it seventh.

Conversely, Audi is having a more positive 2025. The marque was just 2,519 units away from entering the top five. This was thanks to a 6.3% improvement in deliveries across the first six months of the year.

The carmaker’s 100,014 EV sales meant a 5.6% share during the first half, down from 6.5% 12 months ago. This drop could be due to the success of VW, which leads the table.

Elsewhere in the group, Skoda saw sales soar as it moved up one spot to seventh. It enjoyed the biggest year-on-year increase of the top 10 brands, with a 154.4% jump to 91,943 units. Its share more than doubled, going from 2.5% to 5.1%. Its second quarter was also exceptional, with a 199.2% rise in deliveries.

Cupra and Kia drop

In turn, Cupra dropped one position to eighth. The Spanish marque saw triple-digit growth in the first quarter, with volumes up 124.6% from January to March. It could not match this performance in the second quarter, but still recorded a 56.4% increase.

This equated to an 84.6% improvement in the first half of the year, while its share rose from 2.9% to 4.3%.

Renault was another manufacturer that started the year well, with a 90% year-on-year rise in volumes during the first quarter. Its sales pace slowed slightly from April to June, as it recorded a 57.9% rise.

This equated to a 72% delivery increase in the first half of 2025, which was enough for it to move into ninth. Accordingly, its market hold rose by 1.1pp to 4.1%.

Kia dropped to 10th, with its 72,457-unit total up 12.5% compared to the first half of 2024. Despite its consistent growth, its share fell from 4.4% to 4%. This decline can be attributed to increased competition and strong sales improvement from other brands.

The brand’s position in the top 10 does not appear secure. Kia was the 12th best-selling EV carmaker from April to June, while BYD came eighth. This marked the Chinese carmaker’s first appearance in Europe’s quarterly table. The Chinese marque enjoyed the biggest year-on-year increase of any brand in the top 10 in the second quarter. Its sales grew by 335.6% to 42,005 units. BYD could enter the annual chart in the third quarter if its sales keep following this trend.

The content is presented to you by Autovista24